title to the Warehouses. The Properties are located in 37 U.S. states and Puerto Rico. In the aggregate, the Warehouses and Retail Properties comprise 10.1 million square feet and 21.7 million square feet, respectively, of leasable space, all of which is leased to the tenants under the Master Leases. See “Item 3. Properties” for a detailed description of the Properties.

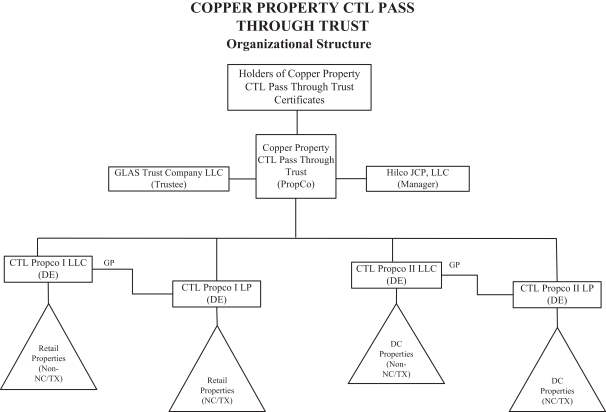

The following organizational chart describes the organizational structure of the Trust as of the effective date of this registration statement. See Exhibit 21.1 to this registration statement for a list of subsidiaries of the Trust.

Business

The Trust exists for the sole purpose of collecting, holding, administering, distributing and monetizing the Properties for the benefit of Certificateholders.

The Trust’s operations consist solely of (i) owning the Properties, (ii) leasing the Properties to New JCP (who will operate the premises pursuant to the Master Leases, including for warehousing, distribution and retail operations), and (iii) subject to market conditions and the conditions set forth in the Trust Agreement (as further described under “—Description of the Trust Documents—Trust Agreement”), selling the Properties from time to time to third-party purchasers as promptly as practicable, in each case through the PropCos. Except for rental proceeds from leasing the Properties and sales proceeds from selling the Properties, the Trust has no other source of revenue or cash flow. Pursuant to the Trust Agreement, the Trust shall endeavor to complete the disposition of the Warehouses within six months following the Effective Date and the Retail Properties within 12 months following (i) the expiration of any applicable Lockout Periods or (ii) if not subject to such Lockout Period, the Effective Date, or in each case such longer period approved by the Certificateholders representing a majority of the Trust Certificates (the “Majority Certificateholders”). See “—Description of the Trust Documents—Master Leases—Lockout Periods.”

3